Summary: Scope 1 emissions are the direct greenhouse gas emissions a company creates from sources it owns or controls, such as on-site fuel combustion, industrial processes, and company vehicles. For supply chain and ESG teams, accurate Scope 1 emissions data is the foundation for credible carbon accounting, regulatory reporting, and target setting. Clear separation of Scope 1 from Scope 2 and Scope 3 also improves compliance, auditability, and decision-making.

Table of contents

Scope 1, 2, and 3 emissions are the three standardized categories of greenhouse gas (GHG) emissions that businesses measure and report. The World Resources Institute’s Greenhouse Gas Protocol (GHG Protocol) established these categories. As such, this globally recognized framework provides a consistent, transparent structure for corporate emissions accounting. Organizations use it to track, manage, and disclose their full carbon footprint.

In 2025 and beyond, understanding all three scopes is not only a sustainability best practice. It is also a legal requirement under several frameworks. For example, the EU Corporate Sustainability Reporting Directive (CSRD) mandates Scope 3 supply chain emissions disclosure for in-scope companies. Similarly, the Corporate Sustainability Due Diligence Directive (CSDDD) requires environmental impact assessment across global value chains.

Scope 1 Emissions

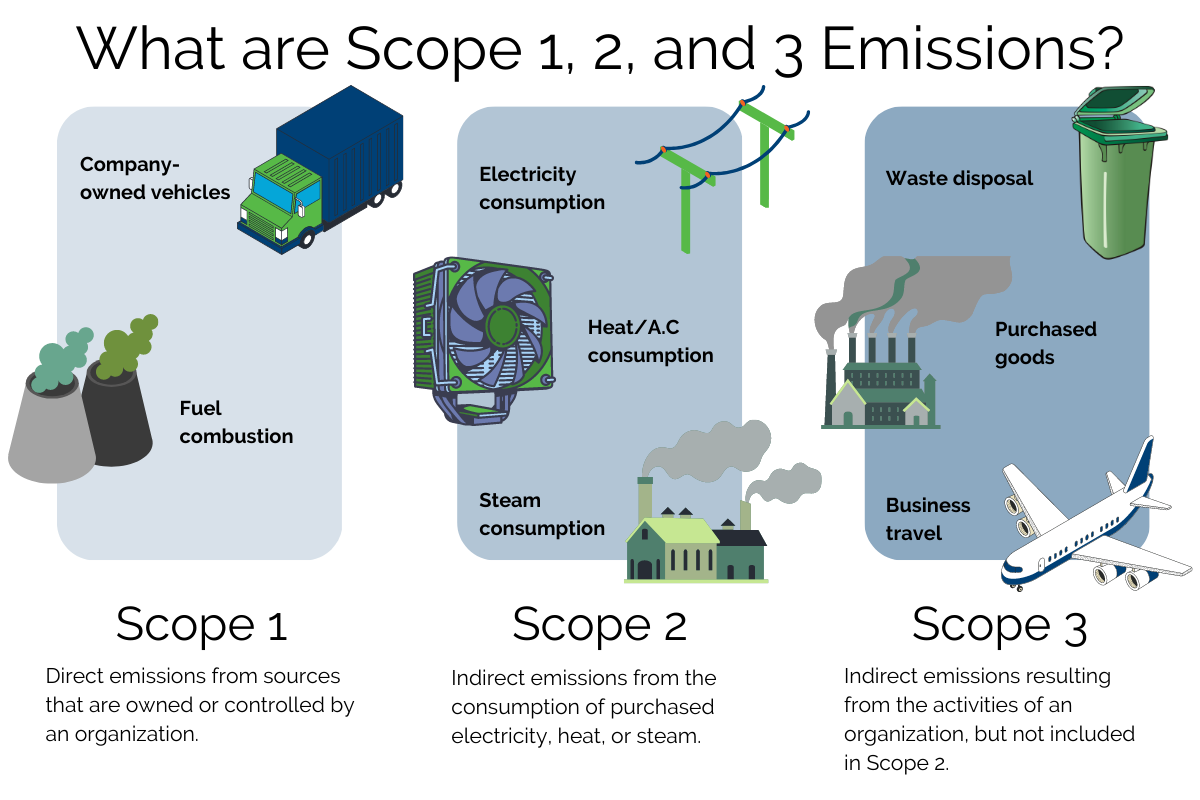

Scope 1 emissions are direct greenhouse gas emissions from sources that an organization owns or controls. In other words, these are emissions the company generates directly through its own operations. Examples of Scope 1 emissions include on-site fossil fuel combustion for heating, cooling, or industrial processes. They also include emissions from company-owned or leased vehicles, known as fleet emissions. Additionally, fugitive emissions from refrigeration and air conditioning systems fall into this category. Process emissions from chemical or manufacturing operations also qualify.

Because Scope 1 emissions are under direct organizational control, they are typically the first target of reduction initiatives. Consequently, most net-zero transition plans prioritize these emissions as a starting point.

Scope 2 Emissions

Scope 2 emissions are indirect greenhouse gas emissions associated with purchased electricity, heat, steam, or cooling. These emissions occur at the point of energy production, not at the reporting organization’s facilities. However, they are a direct consequence of the organization’s energy purchasing decisions.

For example, if a company purchases electricity generated from coal-fired power plants, those generation emissions count as Scope 2. Fortunately, organizations can significantly reduce their Scope 2 footprint. Specifically, they can switch to renewable energy sources, purchase renewable energy certificates (RECs), or sign Power Purchase Agreements (PPAs) with clean energy providers.

Scope 3 Emissions

Scope 3 emissions encompass all other indirect greenhouse gas emissions across an organization’s value chain. These activities are not directly owned or controlled by the reporting entity. Notably, this is by far the largest and most complex emissions category for most companies.

Scope 3 sources include purchased goods and services, capital goods, and fuel-related activities not captured in Scopes 1 and 2. Furthermore, they cover upstream transportation, business travel, employee commuting, and waste disposal. They also include the use of sold products, end-of-life treatment, leased assets, franchises, and investments.

For many industries, Scope 3 represents more than 70% of total GHG emissions. As a result, supply chain engagement is a central pillar of any credible net-zero strategy. Moreover, under the EU CSRD, large companies and listed SMEs must now disclose material Scope 3 emissions. This requirement drives an urgent need for supplier-level emissions data collection.

Want to share this image on your site? Click here to copy and paste the code.

<p><strong>Please include attribution to certaintysoftware.com with this graphic.</strong><br /><br /><a href='https://www.certaintysoftware.com/what-are-scope-1-2-3-emissions/'><img src='https://www.certaintysoftware.com/wp-content/uploads/2023/01/Scope-123-Emissions-Infographic.webp' alt='What are scope 1, 2, and 3 emissions?' width='600px' /></a></p>

Why it’s Important to Understand These Differences

Understanding and actively managing Scope 1, 2, and 3 GHG emissions is essential for organizations across multiple dimensions. First, greenhouse gas emissions are the primary driver of climate change. This creates material environmental, physical, and economic risks for businesses. By reducing emissions across all three scopes, organizations contribute to limiting global warming. Furthermore, they support the transition to a net-zero economy. This transition is increasingly a prerequisite for investor confidence and long-term enterprise value.

30+ Audit and inspection checklists free for download.

Second, managing scope emissions is now a legal compliance obligation for a growing number of companies. The EU Corporate Sustainability Reporting Directive (CSRD) entered into force in 2024 with phased applicability through 2026. Specifically, it requires large companies and listed SMEs to report material Scope 1, 2, and 3 emissions under the European Sustainability Reporting Standards (ESRS). In addition, the CSDDD requires organizations to assess and address environmental impacts throughout their supply chains. Consequently, companies demonstrating meaningful progress in emissions reduction may qualify for green finance incentives and lower cost of capital.

Third, proactive emissions management strengthens brand reputation and competitive positioning. Investors, institutional buyers, consumers, and strategic partners increasingly apply ESG screening criteria. As a result, companies that can credibly report progress against science-based targets are better positioned. They attract capital, win enterprise contracts, and retain top talent. Ultimately, sustainability credentials serve as a key differentiating factor in today’s market.

How to Better Collect Information on Scope 1, 2, and 3 Emissions

GHG accounting is the process of quantifying Scope 1, 2, and 3 emissions. It follows a structured methodology. Start by selecting the appropriate reporting standard. The GHG Protocol is the globally recognized baseline and is required under CSRD/ESRS. Next, define the organizational and operational boundary for your emissions inventory. This determines which entities, facilities, and supply chain activities fall within your reporting scope. Finally, gather activity data and apply relevant emission factors to calculate total GHG emissions for each category.

For Scope 3 in particular, this requires active data collection from suppliers across your value chain. Therefore, engaging your supplier base is critical to accurate Scope 3 reporting. Businesses should work directly with suppliers to encourage adoption of GHG measurement practices. In addition, they should promote the timely sharing of primary emissions data.

This may involve providing guidance on the GHG Protocol Scope 3 Standard. It can also include offering supplier capacity-building resources. Moreover, working with industry associations to establish sector-level emissions benchmarks is valuable. Under CSRD’s ESRS E1 standard, organizations must report Scope 3 emissions using primary supplier data where material and feasible. For this reason, supplier engagement is a compliance activity, not just a best practice.

Businesses should regularly audit the sustainability performance of suppliers using structured checklists. For example, a Supplier Social and Environmental Compliance Checklist is an effective tool. Teams can deploy this checklist internally for on-site assessments. Alternatively, they can distribute it digitally for suppliers to self-complete. As such, it provides a scalable, consistent data collection mechanism across a multi-tier supplier network.

Overall, Scope 1, 2, and 3 emissions represent the full extent of a business’s climate impact. Understanding, measuring, and reducing emissions across all three scopes is essential. Additionally, reporting transparently under frameworks like the GHG Protocol and CSRD is central to building a sustainable organization. Ultimately, this approach creates a more resilient and compliant business in 2025 and beyond.

You may also be interested in:

Software solution for ESG assessments

Frequently Asked Questions (FAQs)

What is the difference between Scope 1, 2, and 3 emissions?

Scope 1 emissions are direct GHG emissions from sources owned or controlled by your organization (e.g., company vehicles, on-site fuel combustion). Scope 2 emissions are indirect emissions from purchased energy (electricity, heat, steam). Scope 3 emissions cover all other indirect emissions across your entire value chain — from raw material extraction through product end-of-life — including supply chain emissions. Scope 3 is typically the largest category and the focus of CSRD reporting obligations.

Why does CSRD require Scope 3 reporting?

The EU Corporate Sustainability Reporting Directive (CSRD) requires Scope 3 disclosure because supply chain and value chain emissions are often the largest contributor to a company’s total climate impact — frequently exceeding Scopes 1 and 2 combined. Transparent Scope 3 reporting enables investors, regulators, and stakeholders to assess a company’s full climate exposure and the credibility of its net-zero commitments. CSRD’s ESRS E1 standard sets the technical requirements for this disclosure.

How can businesses reduce Scope 3 emissions?

Reducing Scope 3 emissions requires active supplier engagement, supply chain redesign, and procurement policy changes. Key strategies include: setting supplier emissions reduction targets; prioritizing low-carbon suppliers in sourcing decisions; collaborating with suppliers to implement energy efficiency measures; shifting to circular economy product designs; and using digital audit and assessment tools to collect primary emissions data across the supply base. Certainty Software supports this process through structured ESG assessment checklists and supplier compliance tracking.

What tools help with GHG emissions data collection from suppliers?

Digital audit and compliance platforms like Certainty Software enable organizations to deploy standardized ESG assessment checklists to suppliers, capture emissions-related data in real time, and consolidate supplier-level GHG data into aggregated Scope 3 inventories. This replaces manual, spreadsheet-based data collection with a scalable, auditable system aligned with GHG Protocol and CSRD/ESRS requirements.