Summary: ESG reporting gives companies a structured way to disclose environmental, social, and governance performance in a form that regulators, investors, and customers can evaluate. The main benefits of sustainability disclosure are stronger compliance readiness, better reputation, clearer risk visibility, and more credible communication of sustainability progress. For supply chain and ESG leaders, disciplined reporting also improves internal data quality and decision-making.

Table of contents

ESG reporting is a structured corporate disclosure that details an organization’s environmental, social, and governance (ESG) commitments, actions, and measured outcomes. Also known as sustainability reporting, ESG reporting has evolved from a voluntary best practice into a regulatory mandate: the EU’s Corporate Sustainability Reporting Directive (CSRD) now requires tens of thousands of companies to publish audited ESG disclosures annually, while the Corporate Sustainability Due Diligence Directive (CSDDD) and Germany’s Supply Chain Act (LkSG) require documented due diligence on supply chain human rights and environmental impacts. According to research by McKinsey, ESG reporting is now a global norm — and in 2025–2026, regulators, investors, and customers increasingly treat robust ESG disclosure as a baseline expectation, not a differentiator.

Benefits of ESG Reporting

Why should your business invest in sustainability disclosure? Here are the core benefits that a well-structured reporting program delivers:

- Enhance your reputation and public image. ESG reporting showcases your positive impact on the environment, society, and governance, and demonstrates your commitment to ethical and responsible business practices. In an era of mandatory CSRD disclosure, organizations with credible, data-backed ESG reports enjoy stronger brand loyalty, customer satisfaction, and employee engagement than those issuing vague sustainability pledges.

- Attract and retain investors. Investors are increasingly integrating ESG data into their capital allocation decisions. Disclosing material ESG risks and opportunities — including supply chain due diligence outcomes required by CSDDD and LkSG — increases transparency and credibility with institutional investors. This reporting process also unlocks access to green bonds, sustainability-linked loans, and other ESG-labelled capital instruments that carry preferential financing terms.

- Reduce risks and improve performance. Systematic ESG reporting helps organizations identify and address environmental and social impacts across their operations and supply chains — including Scope 3 greenhouse gas emissions, supplier human rights risks, waste management gaps, and diversity shortfalls. Proactive identification of these issues mitigates potential legal, regulatory, reputational, and operational risks, and drives efficiency and innovation throughout the business.

- Meet regulatory obligations. Under CSRD, large EU-listed companies and their significant non-EU value chain partners must publish third-party assured ESG reports aligned with the European Sustainability Reporting Standards (ESRS). LkSG requires German-headquartered companies above 1,000 employees to publish an annual due diligence report. CSDDD — with phased enforcement beginning in 2027 — mandates documented human rights and environmental due diligence for companies operating in EU markets. ESG reporting is the documentation backbone of all these obligations.

What are the Components?

ESG reporting covers three interconnected dimensions of business performance: environment, social, and governance. Each has its own indicators that measure performance and impact. Here are examples of common ESG indicators aligned with major frameworks such as GRI, SASB, and CSRD’s ESRS:

Environment: This dimension covers your organization’s environmental footprint — climate change, biodiversity, water use, waste management, and carbon emissions. Key environmental indicators include greenhouse gas emissions (Scope 1, 2, and 3), energy consumption and renewable energy share, water withdrawal and recycling rate, and waste generation. Under CSRD’s ESRS E1, Scope 3 supply chain emissions are a mandatory disclosure topic for most companies.

Social: This dimension covers how your business affects people — including employees, suppliers, and communities — through human rights, labor practices, health and safety, diversity and inclusion, and community engagement. Key social indicators include employee turnover, gender pay gap, training hours per employee, injury rate, supplier human rights assessment coverage, and social investment spend. LkSG and CSDDD specifically require disclosure on human rights due diligence outcomes within your supply chain, making social reporting a legal necessity for many organizations in 2025–2026.

Governance: This dimension covers how your business is directed and controlled — board composition, executive compensation, business ethics, anti-corruption policies, risk management frameworks, and stakeholder engagement. Key governance indicators include board diversity, CEO pay ratio, code of conduct compliance rate, and supplier audit coverage. Strong governance disclosure underpins investor and regulatory confidence in the integrity of your ESG data and processes.

What are the challenges and opportunities of ESG reporting?

Challenges

The reporting process is not without significant challenges. The most common ones organizations face in 2025–2026 include:

- Data collection and verification. Sustainability disclosure requires collecting and verifying data from multiple sources — internal systems, external providers, supplier surveys, and on-site audits. This is particularly complex for organizations with global, multi-tier supply chains attempting to collect Scope 3 data and CSDDD-required supplier due diligence evidence. Under CSRD, third-party assurance of ESG data raises the bar on data quality, consistency, and auditability.

- Integration and alignment. Integrating ESG information with financial reporting — and aligning it across multiple frameworks such as GRI, SASB, TCFD, and the new ESRS — remains a significant challenge. Different frameworks have different definitions, scopes, and materiality thresholds. CSRD’s double materiality assessment, for example, requires organizations to evaluate both the financial materiality of ESG risks and the impact materiality of their activities on people and the planet.

- Communication and engagement. ESG reporting requires effective communication and engagement with diverse stakeholders — investors, customers, employees, regulators, and civil society — each with different information needs. Organizations operating under LkSG are also required to establish grievance mechanisms and report on complaints received, adding a structured stakeholder engagement dimension to their reporting obligations.

Opportunities

These challenges present concrete opportunities for organizations that invest in robust sustainability disclosure infrastructure:

- Data-driven decision making. ESG reporting enables organizations to use data to inform strategic decisions on sustainability, supply chain risk, and stakeholder priorities. Well-structured ESG data helps identify and prioritize material risks and opportunities, set SMART targets and KPIs, monitor progress, and evaluate impact — creating a foundation for continuous improvement aligned with CSDDD and CSRD obligations.

- Frameworks and standards adoption. Organizations that adopt recognized ESG reporting frameworks — such as the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), the Task Force on Climate-related Financial Disclosures (TCFD), and the International Integrated Reporting Council (IIRC) — build credibility and comparability. In 2025–2026, alignment with the EU’s European Sustainability Reporting Standards (ESRS) under CSRD is the highest-priority framework adoption for companies operating in or supplying into EU markets.

- Stakeholder relationships building. Transparent, data-backed ESG reporting builds trust with investors, customers, regulators, and communities. Organizations that go beyond compliance minimums — disclosing supply chain due diligence outcomes and grievance mechanism data as required by CSDDD — differentiate themselves as genuinely responsible business partners and reduce the risk of reputational incidents.

How Accenture Integrated ESG and Financial Reporting

One of the leading best practices for ESG reporting is the full integration of sustainability and financial disclosures. Integrated reporting demonstrates how ESG performance connects to business strategy and value creation — a requirement that CSRD’s double materiality framework is now embedding into regulatory expectations.

A landmark example is Accenture, the global professional services company. Accenture launched its 360° Value Reporting Experience in 2021, bringing together all ESG and financial metrics, progress, and performance into a single, coherent reporting experience accessible to all stakeholders.

Accenture achieved this through a cross-functional team and ecosystem partners, creating a comprehensive and transparent reporting experience. It leveraged technology and data to measure and communicate ESG impact across multiple dimensions of value — from client outcomes and workforce equity to environmental targets and supplier standards.

The 360° Value Reporting Experience demonstrates how ESG and financial reporting, when fully integrated, reinforce each other: ESG data informs investor confidence while financial performance data contextualizes sustainability investments. By integrating reporting in this way, Accenture demonstrates its commitment to stakeholder capitalism and positions itself ahead of CSRD’s integrated reporting requirements.

You can learn more about Accenture’s 360° Value Reporting Experience here.

Best Practices and Tips

ESG reporting is not a one-size-fits-all process. Each business has its own regulatory context, stakeholder expectations, and material issues. However, the following best practices consistently improve reporting quality and credibility in 2025–2026:

Identify your material issues

ESG reporting should focus on the issues most relevant and significant for your business and stakeholders. Use a double materiality assessment — as required by CSRD — to identify and prioritize your ESG metrics, evaluating both the financial materiality of ESG risks to your business and the impact materiality of your activities on the environment and society. Free tools like Certainty’s downloadable ESG compliance checklist are a practical starting point for identifying material issues quickly.

30+ Audit and inspection checklists free for download.

Set your targets and KPIs

ESG reporting should include clear, measurable targets and KPIs for each material issue, along with transparent progress tracking. Use SMART criteria — specific, measurable, achievable, relevant, and time-bound — to set targets aligned with your business strategy, regulatory obligations (such as CSDDD supply chain due diligence timelines), and global sustainability agendas like the UN Sustainable Development Goals and the Paris Agreement.

Seek assurance

ESG reporting should be independently verified to ensure accuracy, reliability, and credibility. Under CSRD, limited assurance of ESG disclosures is mandatory, with requirements expected to escalate to reasonable assurance in subsequent reporting cycles. Engage external assurance providers — auditors, specialist consultants, or ESG rating agencies — to review your data, processes, and reports. Assurance also helps identify gaps and improvement opportunities in your reporting practices.

Engage stakeholders

ESG reporting should be a collaborative process involving stakeholders throughout the reporting cycle. Engage them through surveys, interviews, workshops, or webinars to gather input on material issues, reporting quality, and stakeholder expectations. Under CSDDD and LkSG, meaningful engagement with affected communities and workers — including through grievance mechanisms — is a regulatory obligation, not just a best practice.

Report on your impact and value creation

ESG reporting should go beyond inputs and outputs to document outcomes and real-world impacts. Report on how your ESG activities contribute to value creation for your business and stakeholders, and to global sustainability goals. Disclose both positive and negative impacts — including supply chain human rights and environmental impacts as required by CSDDD — and explain how you manage and mitigate them. Use impact measurement methods such as ESG scores to quantify and communicate your contributions.

How to get started with ESG reporting with Certainty

ESG reporting is a challenging and complex undertaking — particularly for organizations new to it, those facing mandatory CSRD or LkSG obligations for the first time, or those with complex global supply chains requiring CSDDD-aligned due diligence documentation. A reliable ESG assessment software solution can simplify and streamline your reporting process while ensuring the data quality and audit trails required by regulators and assurance providers.

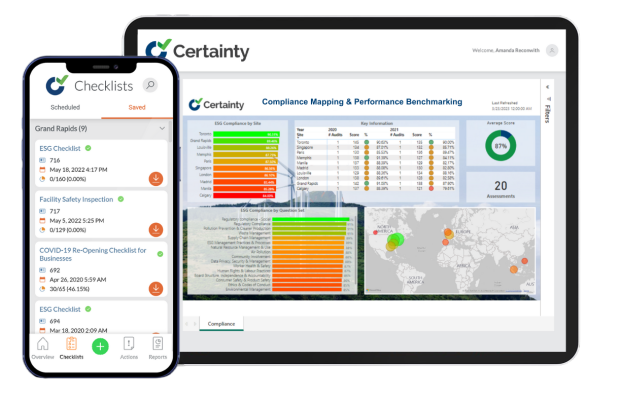

Certainty is a cloud-based software solution that enables businesses to collect, manage, and report on their ESG data and performance — across operations and their entire supply chain. With Certainty, you can:

- Collect ESG data from multiple sources — internal systems, supplier self-assessments, on-site audits, and third-party providers — using customizable forms and templates aligned with CSDDD, LkSG, and CSRD requirements.

- Manage ESG data in a centralized, secure database where you can store, organize, validate, and analyze your data to support regulatory reporting and investor disclosures.

- Report on ESG performance using interactive dashboards and reports that visualize compliance status, benchmark suppliers, and generate disclosure-ready outputs.

- Follow recognized ESG frameworks and standards — GRI, SASB, TCFD, IIRC, and CSRD’s ESRS — using pre-built or custom indicators and metrics.

- Support assurance of your ESG reports through built-in audit trails, evidence management, and verification features.

- Engage stakeholders in your ESG reporting process using built-in collaboration and communication tools, including supplier portals and grievance tracking.

Certainty is designed to make ESG reporting more effective, efficient, and impactful — whether you are a small business beginning your sustainability journey or a large enterprise managing complex CSDDD and CSRD compliance obligations. If you want to learn more about how Certainty can help with your ESG reporting, sign up for a quick demo.

Frequently Asked Questions (FAQs)

What is ESG reporting?

ESG reporting is a structured disclosure by an organization of its environmental, social, and governance performance — including metrics on carbon emissions, labor practices, supply chain human rights, board diversity, and anti-corruption controls. In 2025–2026, ESG reporting is a legal requirement for many large companies under the EU’s CSRD, LkSG, and CSDDD frameworks.

What is CSRD and who does it apply to?

The Corporate Sustainability Reporting Directive (CSRD) is an EU regulation that requires large companies — and eventually SMEs listed on EU regulated markets — to publish audited sustainability reports aligned with the European Sustainability Reporting Standards (ESRS). CSRD uses double materiality, requiring disclosure of both the financial impact of ESG risks on the company and the company’s impact on people and the environment, including through the supply chain.

How does LkSG relate to ESG reporting?

Germany’s Supply Chain Due Diligence Act (LkSG) requires companies with 1,000 or more employees in Germany to publish an annual due diligence report documenting how they identify, prevent, and remediate human rights and environmental risks in their supply chains. This report is a mandatory component of ESG disclosure for in-scope organizations and must be submitted to Germany’s Federal Office for Economic Affairs and Export Control (BAFA).

What ESG reporting frameworks should my company use?

For companies operating in or supplying into EU markets in 2025–2026, alignment with the European Sustainability Reporting Standards (ESRS) under CSRD is the highest-priority framework requirement. Beyond CSRD, organizations commonly report against GRI Standards for global stakeholder disclosure, SASB for industry-specific financial materiality, and TCFD for climate-related risk disclosure. Many organizations use multiple frameworks simultaneously to address different stakeholder needs.

You might also be interested in: