Summary: ESG measures how a company manages its environmental impact, social responsibilities, and governance practices across the business and its supply chain. What is environment, social, governance in practice? It is a framework for identifying risk, improving accountability, and meeting rising expectations from regulators, investors, customers, and suppliers. Companies that operationalize ESG strengthen compliance, trust, and long-term business resilience.

What is Environment, Social, Governance – ESG?

Environment, social, governance (ESG) is the measurement of the positive and negative impact a business has on the environment and on society. It also includes an assessment of governance practices that affect all stakeholders — shareholders, employees, suppliers, customers, and communities. Indeed, first coined in 2004, ESG has evolved from an investment decision-making framework into a comprehensive business management and regulatory compliance imperative. In 2025–2026, ESG performance is directly linked to legal obligations under the EU Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), and Germany’s Supply Chain Due Diligence Act (LkSG). As a result, robust ESG assessment and reporting is now a strategic and compliance necessity for companies of all sizes operating in global markets.

Investing in businesses that embrace ESG — often called sustainable investing, responsible investing, impact investing, or socially responsible investing (SRI) — has become mainstream across institutional and retail capital markets globally.

ESG was first articulated in the landmark 2004 report Who Cares Wins. This collaboration involved the UN Global Compact, the International Finance Corporation, and the Swiss Government. Notably, the report established that integrating environmental, social, and governance factors into corporate reporting and investment decision-making generates better long-term outcomes. Specifically, these benefits extend to capital markets, companies, and society alike. Although initially focused on investment analysis, ESG now increasingly shapes the decisions of employees, customers, policymakers, and regulators.

The foundation of best practice ESG reporting is a rigorous assessment of ESG performance against environmental, social, and governance criteria. In essence, this process functions as an ‘ESG SWOT analysis’ that identifies risks and opportunities. Furthermore, improved ESG performance comes through governance practices that effectively identify, manage, and mitigate the social and environmental risks of a business and its supply chain.

At its core, ESG is a tool to measure the sustainability of a business and its long-term return on investment. Ultimately, improved ESG performance makes a business more sustainable and strengthens capital markets. Additionally, it builds supply chain resilience and delivers better outcomes for the societies and environments on which we all depend.

How is ESG Performance Assessed?

No single globally accepted ESG assessment standard exists today. However, all ESG performance assessments attempt to measure the impact a business has on the environment and society. Additionally, they evaluate how well the business governs and manages those impacts. In practice, leading frameworks such as the GRI Universal Standards, the IFRS Sustainability Disclosure Standards (ISSB), and the European Sustainability Reporting Standards (ESRS) under CSRD provide structured, comparable methodologies. Notably, these frameworks are increasingly converging toward a common global approach.

Environment

Environment assesses the impact a business has on the natural environment. This includes the full lifecycle impacts of its products and services — from raw material sourcing through production, use, transportation, and disposal. Under CSRD and the ESRS, environment assessments must now include double materiality analysis. In other words, this analysis considers both the financial risks that environmental factors pose to the business and the impacts the business has on the environment. Environment should include an assessment of:

- natural resources sourcing, use, management, and conservation

- impact on biodiversity and the treatment of animals

- air pollution – especially greenhouse gas (GHG) emissions and carbon footprint, including Scope 1, 2, and 3 emissions

- waste management and discharges to land and water

- the use of toxic chemicals and the management of hazardous waste

- energy use and conservation

- environmental risks and how well those risks are managed (contaminated land, natural disasters, climate change, etc.)

- compliance with environmental regulations, including CSRD environmental disclosure requirements

Social

Social assesses the impact a business has on society and its relationships with stakeholders. These stakeholders include employees, consumers, suppliers, and the communities in which it operates. In 2025–2026, the social dimension has gained particular regulatory urgency. Specifically, CSDDD requires companies to conduct human rights and labor standards due diligence across their supply chains. Similarly, LkSG mandates specific social risk assessments for German-nexus supply chains. Social should include an assessment of:

- respect for and observance of human rights — including the right to a living wage, freedom of association, and prohibition of forced and child labor

- working conditions and fair labor practices – including those of suppliers and the supply chain, as required by CSDDD and LkSG

- hiring practices, employee engagement, equal opportunity, gender, diversity, and inclusion

- occupational health and safety management

- community relations, initiatives, and engagement

- customer satisfaction

- social risks and how well they are managed

- social license to operate (SLO) and meeting the expectations placed on a business for societal acceptance

Governance

Governance assesses how well a business is governed and examines the composition and transparency of its Board of Directors. It also evaluates the degree to which governance practices identify, manage, and mitigate the environmental and social impacts of a business. Under CSRD’s ESRS G1 standard, governance disclosures now include specific requirements around business conduct, anti-corruption, and supply chain due diligence oversight at board level. Governance should include an assessment of:

- board structure, diversity, and independence

- executive selection (including conflict of interest), committees, and compensation

- board transparency and shareholder rights

- board understanding of and commitment to ESG, including oversight of CSDDD and CSRD compliance

- corporate codes of conduct, business ethics, and values (including bribery, fraud, and corruption)

- lobbying and political contributions

- data protection, privacy, and security

- corporate risk management and how well risks are managed (actual and potential lawsuits, supply chain interruptions, natural disasters, regulatory change, loss of reputation and brand value)

- compliance with financial regulations, accounting standards, and disclosure requirements

Why is ESG Important for Companies and Their Boards?

Improved Access to Capital

ESG emerged in 2004 from a collaborative initiative between the UN Global Compact and the CEOs of more than 20 major financial institutions. These institutions held combined assets under management (AUM) of over USD $6 trillion. Importantly, the initiative established that integrating environmental, social, and governance issues into investment decision-making reduces business risk. Moreover, it improves long-term corporate performance and delivers more sustainable outcomes for society.

Since its inception, the growth of ESG-aligned capital has been extraordinary. Between 2016 and 2021, ESG AUM grew at approximately 30% per year. As of 2025, ESG-oriented assets have become a mainstream component of institutional portfolios globally. They now represent a significant and growing share of total AUM. Consequently, businesses with strong ESG performance attract preferential access to this capital. On the other hand, those with poor ESG credentials or inadequate disclosure face increasing exclusion from ESG-oriented investment mandates and higher costs of capital.

In the current regulatory environment, access to capital is further influenced by CSRD compliance. Large EU companies must now publish standardized sustainability reports that investors use directly in their ESG assessment and portfolio allocation decisions. Therefore, companies that fail to produce credible, verified ESG data face both regulatory penalties and capital market disadvantage.

Improved Risk Management

The operating environment has become increasingly complex. Climate change, geopolitical instability, and supply chain disruption now create cascading risks. In response, ESG provides a structured framework for identifying and managing business externalities before they crystallize into financial losses. Environmental and social factors that were once treated as external to business risk are now recognized as material risks to long-term sustainability.

In practice, ESG is the assessment of a company’s risk profile, externalities, and management activities in relation to all its stakeholders. These stakeholders include workers, communities, customers, shareholders, and the environment. It serves as the lens through which investors, regulators, employees, and society evaluate the companies they interact with. Furthermore, under CSDDD, companies are now legally required to assess and manage human rights and environmental risks across their value chains. This effectively embeds ESG risk management into the compliance framework.

Businesses that incorporate ESG best practices into their governance, operations, and culture are, by definition, practicing best-in-class risk management. Consequently, they identify risks earlier and manage them more effectively. As a result, they are better positioned to avoid the reputational, operational, and regulatory consequences of ESG failures.

Better Financial Performance

The 2004 UN Global Compact report Who Cares Wins concluded that improved management of environmental, social, and governance issues would ‘increase shareholder value‘ and ‘have a strong impact on reputation and brands‘. More than two decades of evidence has validated this conclusion across global capital markets.

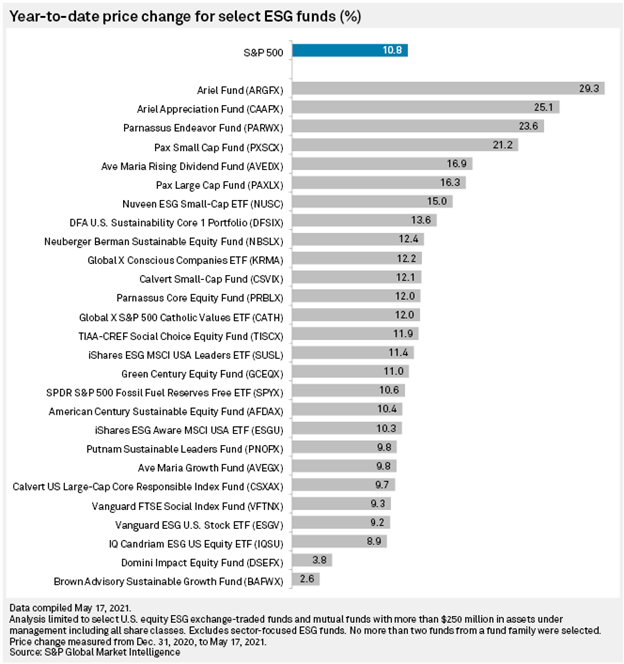

According to S&P Global Market Intelligence, ESG exchange-traded funds and mutual funds have frequently outperformed broader market benchmarks during comparable measurement periods. In fact, this demonstrates that strong ESG performance correlates with financial resilience. Moreover, more recent analyses confirm that companies with high ESG scores tend to exhibit lower volatility, stronger earnings quality, and greater operational durability during periods of market stress.

By incorporating ESG thinking into governance and management, a business regularly and systematically assesses both financial and non-financial factors affecting long-term sustainability. ESG-led businesses therefore have a wider, deeper, and longer-term view of risks and opportunities. Consequently, they are better equipped to recognize and act on them before competitors or regulators force their hand.

Source: S&P Global Market Intelligence

Increasing Risk in Not Embracing ESG

The financial and regulatory risks of ESG laggardship have escalated significantly in 2025–2026. ESG leaders enjoy preferential access to a growing pool of ESG-oriented capital. In contrast, laggards face exclusion, divestment pressure, and in some cases direct regulatory penalties. For example, European asset managers have threatened divestment from companies linked to Amazon deforestation — a dynamic that has only intensified. This illustrates the real-world consequences of inadequate ESG performance and disclosure.

According to Reuters, major European asset management firms with billions in assets have taken concrete steps to divest from companies associated with environmental destruction. Specifically, they act when these companies fail to demonstrate credible ESG progress. Moreover, this pattern has expanded to cover labor rights violations, supply chain controversies, and governance failures.

Beyond investor action, regulatory risk has become concrete and immediate. CSRD now requires approximately 50,000 EU companies to publish audited sustainability reports under the European Sustainability Reporting Standards. This represents a significant expansion from the 12,000 covered by the earlier NFRD. Additionally, CSDDD creates civil liability for companies that fail to conduct adequate due diligence on supply chain impacts. LkSG fines can reach 2% of global annual turnover for companies exceeding €400 million in revenue. For this reason, businesses that delay ESG integration do so at increasingly significant financial and legal peril.

Ensures Compliance with Existing and Impending ESG Reporting Requirements

The ESG regulatory landscape has evolved dramatically since the EU enacted the Non-Financial Reporting Directive (NFRD) in 2014. Specifically, that directive required approximately 12,000 large EU public-interest entities to disclose social and environmental information. However, it has since been superseded by a far more comprehensive framework.

The EU Corporate Sustainability Reporting Directive (CSRD) entered into force in 2023 and is being phased in through 2026. It replaces the NFRD and extends mandatory sustainability reporting to approximately 50,000 companies. CSRD reporting must align with the European Sustainability Reporting Standards (ESRS). These standards cover environmental topics (climate, biodiversity, water, pollution), social topics (workforce, supply chain workers, communities, consumers), and governance topics. Furthermore, reports must be audited by an independent assurance provider. This raises the bar for data quality and internal controls significantly.

The EU Corporate Sustainability Due Diligence Directive (CSDDD), adopted in 2024, goes further by requiring companies to act on identified ESG risks — not just disclose them. Specifically, CSDDD mandates that covered companies identify, prevent, mitigate, and remediate adverse human rights and environmental impacts across their value chains. In practice, this obligation directly links ESG performance measurement to supply chain management. As a result, robust supplier audit and assessment programs become a legal requirement rather than a voluntary best practice.

Germany’s LkSG (Lieferkettensorgfaltspflichtengesetz) has been in force since 2023 for companies with 1,000+ employees in Germany. It requires documented risk analysis, preventive measures, and remediation processes for human rights and environmental risks across direct and indirect supply chains. Notably, this law establishes a national template that other EU member states are now following.

30+ Audit and inspection checklists free for download.

At the international level, the IFRS Foundation’s International Sustainability Standards Board (ISSB) has published IFRS S1 and IFRS S2. These are the first globally comparable sustainability disclosure standards. They are now being adopted or referenced by regulators in more than 20 jurisdictions. Similarly, the SEC’s climate disclosure rules (subject to ongoing legal review in the US) reflect the global direction of travel toward mandatory, standardized ESG reporting.

The regulatory trajectory is clear: ESG disclosure requirements are becoming more comprehensive, more standardized, and more enforceable. Therefore, companies that build robust ESG measurement and reporting infrastructure now will be far better positioned to meet current obligations. They will also adapt to further regulatory evolution without disruptive compliance sprints.

What is Best Practice ESG Reporting?

In 2025–2026, best practice ESG reporting means producing structured, verified, decision-useful sustainability disclosures aligned with recognized international standards. For EU companies, this also means complying with mandatory ESRS reporting under CSRD. While full standardization is still developing, several reporting frameworks define the current gold standard:

The Global Reporting Initiative Universal Standards

Established in 2000, the Global Reporting Initiative (GRI) remains the world’s most widely used sustainability reporting framework. It features 35 Universal Standards and a growing set of Sector Standards now covering 45 industries. GRI Standards enable organizations to communicate their most significant impacts on the economy, environment, and people. This forms the basis of GRI’s materiality approach. Importantly, the ESRS required under CSRD were developed with interoperability with GRI in mind. Consequently, GRI reporters have a significant head start on CSRD compliance.

The Value Reporting Foundation, Integrated Reporting <IR> Framework, and SASB Standards

The Value Reporting Foundation — which consolidated with the IFRS Foundation in 2022 — developed both the Integrated Reporting <IR> Framework and the 77 industry-specific SASB Standards. SASB Standards address sustainability-related risks and opportunities that are financially material for specific industries. For this reason, they are particularly useful for investor-focused ESG reporting. Moreover, the ISSB’s new IFRS S1 and S2 standards have drawn heavily on SASB’s industry-based approach. As a result, SASB alignment remains best practice for organizations seeking capital market credibility.

The convergence of reporting frameworks — driven by ISSB, CSRD/ESRS, and the ongoing harmonization efforts of GRI, TCFD, and CDP — is creating an increasingly integrated global ESG reporting architecture. Companies that invest in building high-quality ESG data collection infrastructure will therefore be well positioned. Similarly, those with robust supply chain ESG assessment processes and credible third-party assurance capabilities will meet evolving requirements without repeated compliance reinvestment.

Frequently Asked Questions (FAQs)

What is the difference between ESG and CSR?

Corporate Social Responsibility (CSR) is a broad, often voluntary framework through which companies commit to operating in an ethical, socially responsible, and environmentally sound manner. In contrast, ESG is a more structured, measurable approach. It uses specific environmental, social, and governance metrics to assess corporate sustainability performance. While CSR is largely self-defined by each company, ESG uses standardized criteria that enable comparison across companies. For this reason, investors, regulators, and rating agencies use ESG rather than CSR as their primary assessment framework.

What regulations require ESG reporting in 2025–2026?

The most significant ESG reporting regulations in 2025–2026 include the EU Corporate Sustainability Reporting Directive (CSRD). This directive requires approximately 50,000 companies to publish audited sustainability reports aligned with ESRS. Additionally, the EU Corporate Sustainability Due Diligence Directive (CSDDD) requires large companies to conduct and act on supply chain due diligence. Germany’s LkSG mandates supply chain human rights and environmental due diligence. Furthermore, the IFRS Sustainability Disclosure Standards (S1 and S2) are now adopted or referenced in over 20 jurisdictions. Various national modern slavery reporting acts (UK, Australia, Canada, Germany) also contribute to this regulatory landscape.

How does ESG relate to supply chain management?

Supply chains are a central ESG concern because a company’s most significant environmental and social impacts often occur in its supply chain rather than its own operations. For example, Scope 3 emissions — indirect emissions from the supply chain — typically represent the majority of a company’s total carbon footprint. Moreover, CSDDD and LkSG both require companies to assess and address human rights and environmental risks in their supply chains. Effective supply chain ESG management therefore requires structured supplier assessment, audit programs, and compliance monitoring — capabilities at the heart of what platforms like Certainty Software deliver.

What is the role of ESG software in compliance?

ESG software supports compliance by enabling organizations to collect structured ESG data from their supply chains. It also helps conduct and document supplier assessments, track non-conformances and corrective actions, and aggregate data for CSRD and GRI reporting. Additionally, it generates the audit-ready documentation required by CSDDD and LkSG. Without purpose-built software, managing ESG data at scale across complex supply chains is operationally impractical. Learn more about how Certainty is used by businesses and their supply chains for ESG assessments.

You may also be interested in:

How Certainty is used by businesses and their supply chains for ESG assessments